FHA 232 LEAN

232 New Construction Loans - 232 LEAN Refinance - A Leading lean lender - FHA 232 LEAN new construction loans

Thursday, May 23, 2013

Tuesday, April 30, 2013

Wednesday, March 20, 2013

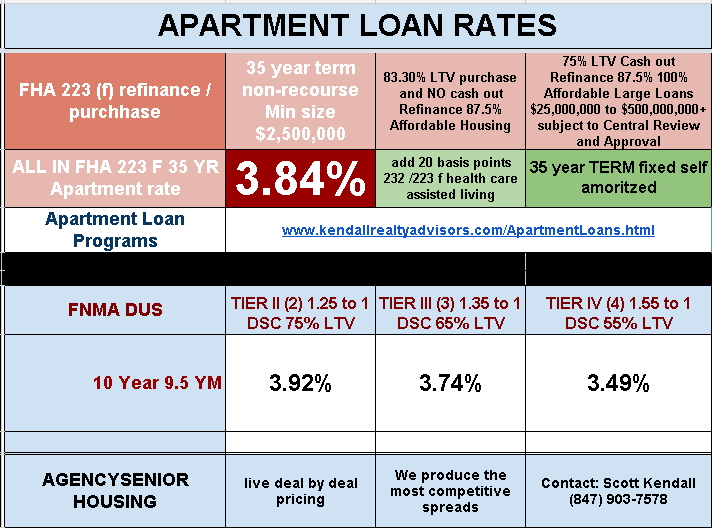

Wednesday, March 6, 2013

FINANCING FOR SENIOR HOUSING, NURSING HOMES, ASSISTED LIVING, AND HOSPITALS

Owners of multifamily, nursing homes, assisted living

facilities, and hospitals have long preferred traditional bank lenders over

FHA-based financing. The usual reason is

the difficulty and frustration of dealing with FHA versus the relative ease of

dealing with sophisticated lenders. Due

to the changes from the real estate market crash, the wave of bank

consolidations, and the reluctance of the remaining banks to return to lending,

owners should reexamine their traditional views of FHA financing.

Traditional financial institutions no longer securitize senior

multifamily and health care loans, thereby eliminating the availability of

conduit financing for these projects. We

have not yet seen the end of the foreclosure crisis and if banks incur addition

losses, bank financing for these types of projects will be almost impossible to

obtain.

FHA, on the other hand, has improved its process

dramatically. FHA-based financing has

always offered several significant advantages over traditional bank and conduit

lending sources if one was willing to deal with the red tape. Much of that red tape has now been removed or

streamlined and programs to finance hospitals have been added. The most obvious advantage to FHA is

continued credit availability that is unaffected by the subprime fiasco. Additional advantages are lower fixed rates,

nonrecourse loans, and long-term fully-amortizing debt.

FHA loans do not contain the numerous covenants contained in

traditional lending documents and specifically do not contain a debt service

coverage requirement. As markets evolve

and Medicaid and Medicare reimbursement methodologies are revised, a manager’s

ability to maintain a stable and predictable debt service coverage is

continually challenged. FHA-based

financing will prove especially valuable.

Charles Kendall 773-259-7074

kendallrealtyadv@gmail.com

Scott Kendall 847-903-7578

kendallrealty@gmail.com

Wednesday, May 30, 2012

Record low #Apartment #Loan #apartmentLender #Apartment Loan

RECORD LOW APARTMENT LOAN RATES

rates

As rumors of LEFTIST gaining popularity in Greece over REVOLT OVER AUSTERITY

everyone buys US currency and stashes it in their pillow. THE normal suspects go down as dollar gains in value oil, interest rates and stocks go down on fright to safety moves

Stocks fell sharply Wednesday as worries about Europe's debt, specifically the Spanish banking system,again shook confidence.

Investors flooded into U.S. Treasuries, raising prices and pushing the yield on the benchmark 10-year note down to a record low of 1.656%.

The Dow Jones industrial average (INDU) was down 150 points, or 1.2%, in early trading. The S&P 500 (SPX) sank 17 points, or 1.2%, and the Nasdaq (COMP) declined 38 points, or 1.3%.

The European Central Bank issued a statement Wednesday saying it had not been consulted on the bailout for Bankia, the No. 4 bank in Spain, and that such a recapitalization could not be provided by the Eurosystem.

In addition, independent ratings agency Egan-Jones downgraded Spain's sovereign debt late Tuesday. The move raised more questions about the country's ability to fund bank bailouts that could reach as much as €100 billion.

Yields on 10-year Spanish debt soared to 6.62% Wednesday.

In addition, the European Commission's economic sentiment index fell for the second month in a row, hitting the lowest level since October 2009.

World markets were sharply lower on European concerns. Britain's FTSE 100 (UKX) dropped 1.6% in afternoon trading, the DAX (DAX) in Germany lost 1.3% and France's CAC 40 (CAC40) plunged 1.7%.

CNNMoney's Fear & Greed Index, which measures investor sentiment, remains firmly in "extreme fear" territory.

U.S. stocks ended higher Tuesday, as investors welcomed a lack of negative headlines out of Europe and hopes that China would announce a new massive stimulus program

Thursday, May 24, 2012

commercial property, prices recovered to mid-2003 Levels CoStar 2012 News APARTMENT LOAN RATES LINK

APARTMENT LOAN RATES LINK

Despite a generally flat March for pricing of commercial property, prices recovered to mid-2003 levels in the first quarter as improving fundamentals and liquidity causing a broadening of the recovery into non-core commercial real estate and secondary markets, according to this month's CoStar Commercial Repeat Sale Indices (CCRSI) report.

At this rate it will be 2006 in ten short years. Oprah sells her Chicago condo for about 1/2 of what she paid. say $3,000,000 on $6,000,000 cost plus extra shoe closets.

Wednesday, May 23, 2012

Subscribe to:

Posts (Atom)